The Price of Being Political

A new study indicates politically lopsided C-suites hurt their firms’ stock performance.

Top bosses always say they want their senior team to be in total alignment. Generally, that’s great for performance, except in one surprising instance.

In a new study from three finance professors, senior leadership teams whose politics didn’t strongly lean one way or another were better for shareholders than teams that were in political lockstep. Indeed, the more partisan the executive team, the more money shareholders lost—in some cases hundreds of millions of dollars.

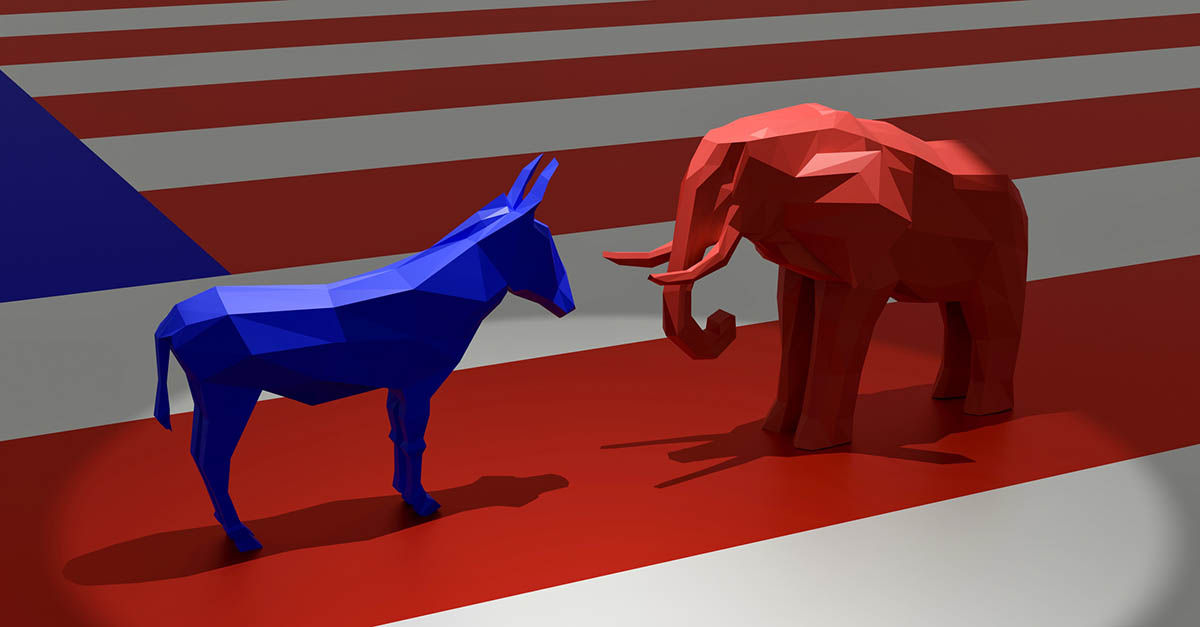

These findings come at a time when C-suites everywhere are increasingly being asked to take stands on social and political issues. Some investors and consumers boycott firms that don’t. People tend to hire those who share their political views, so “over time, executive teams have become more partisan,” says Vyacheslav Fos, a professor at Boston College and one of the study’s co-authors.

Experts say that uniform political leanings in the C-suite could end up creating an autocratic environment in which the top boss makes decisions and the other C-suite members unquestioningly execute them. “If it’s a polarized political environment, it can be a polarized decision-making,” says David Vied, leader of Korn Ferry’s Medical Devices and Diagnostics practice.

Using voter-registration data, the researchers identified the party affiliations of the five most highly-compensated executives at each of 941 midsize and large publicly traded firms between 2008 and 2020. (Voter registrations tend to align more closely with individuals’ political views than do political contributions, which can be made for a variety of reasons.) They ended up with a cohort of nearly 4,000 executives.

For most executive teams, the Republican party was the affiliation of choice: on average, 69% of a firm’s top executives were Republicans and 31% were Democrats. Regardless of affiliation, however, the firm’s top teams became more partisan over the thirteen-year period of the study.

The researchers monitored the stock market’s reaction whenever a highly-paid executive left the firm. They then divided each executive departure into two categories. In the first, the executive departure had no impact on the firm’s overall political leanings—meaning that the departing leader had essentially the same affiliation as his C-suite colleagues. In the second category, the departing executive had a different affiliation than their former peers.

The researchers’ findings were striking. Over two trading sessions following executive departures, the average return of stocks in the second group was 1.7 percentage points lower than that of stocks in the first group. That’s a big difference for such a short period, since stocks tend to only move a couple of percentage points in either direction during any given session.

In dollar terms, the inferior performance of the stocks in the second group translated to an average reduction of $238 million in each company’s market cap.

The results of the study add to a growing body of research showing that diversity of all forms has positive effects on decision-making, the speed at which products are brought to market, and overall business performance. “Political diversity is a new frontier in the work of inclusion,” says Andrés Tapia, Korn Ferry’s global strategist for diversity, equity and inclusion.